The trucking industry spent 2023 and 2024 working through the most painful freight market correction in 15 years. A flood of new carrier authorities issued during the 2021–2022 freight boom created massive capacity oversupply just as consumer spending shifted from goods back to services and inventory destocking rippled through supply chains. Rates fell. Carrier exits accelerated. The market reset.

2025 marked the early signs of recovery. 2026 looks like the year that recovery becomes tangible for most owner-operators, though the path won't be linear and the headline numbers will mask significant variation by equipment type, lane, and business model.

Here's the TruckLeap assessment of what to expect.

The Rate Environment: Where We Are and Where We're Going

The Overcapacity Story Is Changing

The defining fact of the 2023–2024 downturn was carrier overcapacity: too many trucks chasing too few loads. That capacity overhang is finally contracting.

The key metric to watch is carrier exit rate. During the downturn, more carriers exited the market each quarter than entered, but it takes time for that to work through the system. As of late 2025, the supply-demand balance has improved meaningfully. The capacity surplus that compressed rates throughout 2023 and 2024 has largely normalized.

What this means practically: the floor on spot rates has risen. During the worst of the downturn, dry van spot rates on major lanes dipped below $1.60/mile. Those levels are unlikely to return in 2026. The weakest carriers exited, and the ones that remain are running leaner operations.

Rate Recovery: Expectations vs. Reality

The freight market recovery will not look like 2021. Rates won't spike 40% in three months. The recovery in 2026 is more likely to be:

- A 10–20% improvement in average spot rates from 2024 lows

- Gradual tightening as e-commerce volumes grow and industrial activity picks up

- Contract rates lagging spot: shippers locked in low rates during the downturn and many contracts don't renew until mid-2026

Owner-operators should plan around a market that's improving but not booming. That means continuing to optimize costs, not just hoping for rate recovery to solve margin problems. Carriers who work with a professional dispatch service that negotiates above-spot rates are better insulated from the volatility of a gradual recovery. Use TruckLeap's cost-per-mile calculator to identify where your operation has room to improve regardless of market direction.

Fuel Costs: The Wildcard That Changes Everything

Diesel prices are one of the most significant uncontrollable variables in trucking profitability. The correlation between diesel prices and freight rates has weakened. Fuel surcharges on contract freight are supposed to compensate, but spot market rates don't automatically adjust with fuel costs.

What to expect in 2026:

- U.S. diesel prices are forecast to remain in the $3.40–$4.00/gallon range nationally, with significant regional variation

- Refinery capacity additions should limit major upside price surprises

- Geopolitical events remain the primary risk, and a supply disruption could push diesel above $4.50/gallon quickly

How to protect yourself:

- Always calculate loads using current fuel prices, not averages. TruckLeap's fuel cost calculator lets you enter real-time diesel prices for accurate load costing.

- Know your fuel surcharge rate on every contract load and make sure it actually covers your cost at current prices

- Consider fuel-efficient routing on long hauls. A 5% difference in fuel efficiency on a 2,000-mile run saves real money at $3.80/gallon

Demand Drivers: What's Growing and What's Not

E-Commerce Freight Continues to Grow

E-commerce freight volume grew approximately 12% in 2025 and is expected to grow another 10–14% in 2026. This freight has specific characteristics:

- High frequency, smaller shipments: More LTL and partial loads, which benefits carriers who can handle mixed freight

- Tight delivery windows: Next-day and same-day expectations from consumers push up the value of reliable carriers

- Returns logistics growth: Reverse logistics (consumer returns) is one of the fastest-growing freight categories, often overlooked by carriers who could capture this volume

The Amazon Relay program is the most direct way for owner-operators to access e-commerce freight volume. It won't pay the highest rates, but it provides consistent volume in a growing category.

Industrial and Manufacturing: Cautiously Positive

Manufacturing activity has been uneven since the pandemic. The industrial outlook for 2026 is cautiously positive:

- Nearshoring and reshoring: Companies moving supply chains closer to the U.S. are generating new domestic freight corridors. Texas, the Southeast, and the Midwest are primary beneficiaries. The Chicago to Dallas lane is one corridor seeing above-average volume growth as Midwest manufacturers shift production closer to the Gulf.

- Infrastructure spending: The continuing rollout of federal infrastructure investments is driving construction material freight, which is favorable for flatbed carriers.

- Automotive: EV production ramp-up and traditional auto production are both generating freight. Flatbed carriers in the Midwest and Southeast should see solid demand.

Retail: Post-Holiday Normalization

Retail freight in 2026 follows the expected seasonal pattern: Q4 peak, Q1 correction, moderate recovery through the year. The key variable is consumer confidence. If inflation continues to moderate and employment stays strong, retail freight will hold up. If economic conditions deteriorate, retail is the first category to slow.

ELD and Regulatory Environment

The ELD (Electronic Logging Device) mandate is fully implemented, with no new surprises there. The regulatory focus in 2026 is on:

- Broker transparency regulations: Proposed rules requiring brokers to disclose their margin on loads. If implemented, this could shift negotiating power toward carriers on the spot market.

- Speed limiter rules: The FMCSA has been pursuing mandatory speed limiters (60–65 mph) for CMVs over 26,000 lbs. This remains contested and may see final rulemaking in 2026. If implemented, it affects productivity on long-haul operations.

- Driver shortage: The driver shortage hasn't disappeared; it's been masked by reduced demand. As freight volume grows in 2026, driver availability will become a constraint again, which is structurally supportive of rates.

Equipment Type Outlook: Who Wins in 2026

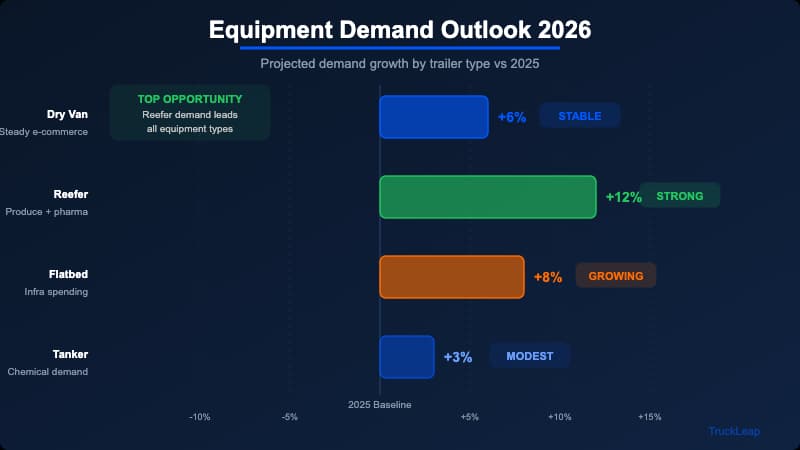

Dry Van

Outlook: Steady improvement

Dry van is the most competitive equipment category but also the highest-volume one. Rate recovery in 2026 will be moderate, enough to improve margins from the 2023–2024 lows, but not a return to 2021 rates.

Owner-operators running dry van should focus on lane efficiency and reducing deadhead. The rate environment rewards operational excellence more than it rewards chasing the highest-paying spot loads. Use TruckLeap's load profitability calculator to evaluate every load, not just the posted rate.

TruckLeap's dry van dispatch service specializes in finding consistent dry van loads at above-spot-market rates through broker relationships built over years.

Reefer

Outlook: Strong, especially during produce season

Reefer is positioned well for 2026. The equipment shortage in reefer (fewer carriers entered reefer during the boom, fewer reefer carriers exited during the downturn) means capacity is tighter relative to demand. Produce season will generate the same rate spikes it always does, and the general reefer market is healthier than dry van.

The caution: reefer maintenance costs are higher and the seasonal volatility is real. Winter months in reefer can be lean. Carriers need cash reserves to bridge the gap.

Flatbed

Outlook: Best positioned for 2026 growth

Flatbed is arguably the best-positioned equipment type for 2026. Three factors converge:

- Infrastructure spending generates construction material freight

- Manufacturing reshoring adds industrial freight in flatbed-heavy corridors

- Flatbed capacity didn't inflate as much as dry van during the boom, so there's less oversupply to work through

Average flatbed rates are expected to improve 12–18% from 2024 lows. Carriers positioned in industrial Midwest lanes and Southeast construction corridors will outperform.

If you're running flatbed and want experienced dispatch, TruckLeap's flatbed dispatch service focuses on the industrial lanes where flatbed rates are strongest.

What Owner-Operators Should Do Now

The improving market creates opportunity, but the owners who win in 2026 are the ones who prepared before the recovery fully arrived. Specific actions:

-

Lock in favorable insurance rates: Insurance markets have softened slightly. Renew or renegotiate before rates firm up again with increased freight activity.

-

Establish contract freight relationships: Spot rates are recovering but contract freight provides the consistency to plan and optimize. Start having rate conversations with shippers now, before the market tightens further.

-

Understand your actual cost structure: Many owner-operators have been absorbing cost increases over the past two years without fully quantifying them. Run a fresh cost-per-mile analysis before you set your 2026 rate floor.

-

Consider professional dispatch: In a recovering market, the difference between a well-negotiated rate and a spot market rate expands. A dispatcher with established broker relationships captures that spread. View TruckLeap's dispatch pricing and apply here if you want to enter 2026 with professional freight support.

Frequently Asked Questions

When will trucking rates return to 2021 levels?

Most analysts do not expect a return to 2021 peak rates, which were historically anomalous. The supply-side correction that occurred in 2023–2024 has created a healthier baseline, but structural conditions (fuel costs, driver wages, equipment costs) mean carriers need better rates than pre-pandemic to be profitable. The "new normal" is likely $0.30–$0.50/mile above pre-pandemic rates on most lanes.

Which states will see the most freight growth in 2026?

Texas, Florida, Georgia, and the Carolinas are expected to outperform in 2026 freight growth, driven by population migration, manufacturing investment, and port activity. Carriers positioned in the Atlanta freight market and the Houston area are well-placed to capture this growth. The industrial Midwest (Ohio, Michigan, Indiana) should also see above-average growth tied to manufacturing and infrastructure.

Is the driver shortage real in 2026?

Yes, though it's been partially masked by reduced freight demand. The American Trucking Associations estimates a shortage of 60,000+ drivers that will grow as freight volume expands. This is structurally positive for rates over the medium term.

Should I expand my fleet in 2026?

Expansion makes sense for owner-operators with strong cash flow, consistent contract freight, and a proven operational model. Expanding speculatively into a recovering spot market is higher risk. The recovery could be slower or more uneven than expected. Build a strong single-truck operation first, then expand from a position of strength.

How do I track diesel prices to manage my costs?

The U.S. Energy Information Administration (EIA) publishes weekly retail diesel prices by region. TruckLeap's fuel cost calculator is updated with current EIA data so you can calculate real-time fuel costs for any load.